Turning 40 in the UK brings many celebrations, but for personal finance enthusiasts, it marks a particularly poignant deadline: the final day you can open a Lifetime ISA (LISA) and access up to £33,000 in government bonuses. With the average age of first-time buyers now reaching 34 (DLUHC, 2024) and retirement planning often starting in one’s 40s, thousands of Britons find themselves confronting this arbitrary age barrier just as their financial planning becomes most urgent.

HMRC data reveals a telling pattern: LISA subscriptions peak at ages 38-39, with a frantic rush to open accounts before the deadline. In the 2022/23 tax year alone, over 85,000 individuals aged 38-39 opened LISAs, representing 42% of all new accounts. This “last-minute surge” demonstrates both the product’s appeal and the frustration of its age-based exclusion.

For the 15.3 million Britons aged 40-49 (ONS, 2024), the question isn’t merely academic—it’s financially significant. This comprehensive guide explores what happens to LISA strategy after 40, examines whether existing accounts remain valuable, and reveals superior alternatives for mid-life savers.

Chapter 1: The Reality Check – What Actually Changes at 40?

The Legal Framework: Age-Based Restrictions Demystified

Many over-40s harbour misconceptions about their LISA eligibility. Let’s clarify what the legislation actually states:

Before 40th Birthday:

- Can open a new LISA (until 11:59 pm on the day before the birthday)

- Can contribute £4,000 annually (until age 50)

- Eligible for a 25% government bonus on contributions

After 40th Birthday:

- ❌ Cannot open a new LISA (absolute cut-off)

- ✅ Can continue contributing to existing LISA until 50

- ✅ Still receive 25% bonus on contributions

- ✅ Can transfer between providers

The Birthday Timing Quirk

Your 40th birthday falls on June 15th? Your final opportunity to open a LISA is June 14th. HMRC uses exact dates, not “in your 40th year.” This catches out hundreds annually who mistakenly believe they have until their birthday.

The Existing Account Advantage

If you opened a LISA at 39, you would enjoy a unique 11-year contribution window (40-50). This creates what financial planners call the “compressed bonus period”:

Example – Sarah opens LISA at 39:

– Years 39-49: 11 contribution years

– Maximum contributions: £44,000

– Maximum bonuses: £11,000

– Potential growth (5% annually): £15,832

– Age 60 value: £70,832

Chapter 2: The Mathematics of Late-Stage LISA Contributions

The “Last Minute” Contribution Analysis

For those with existing LISAs, continuing contributions after 40 requires strategic calculation. The opportunity cost changes significantly in your 40s.

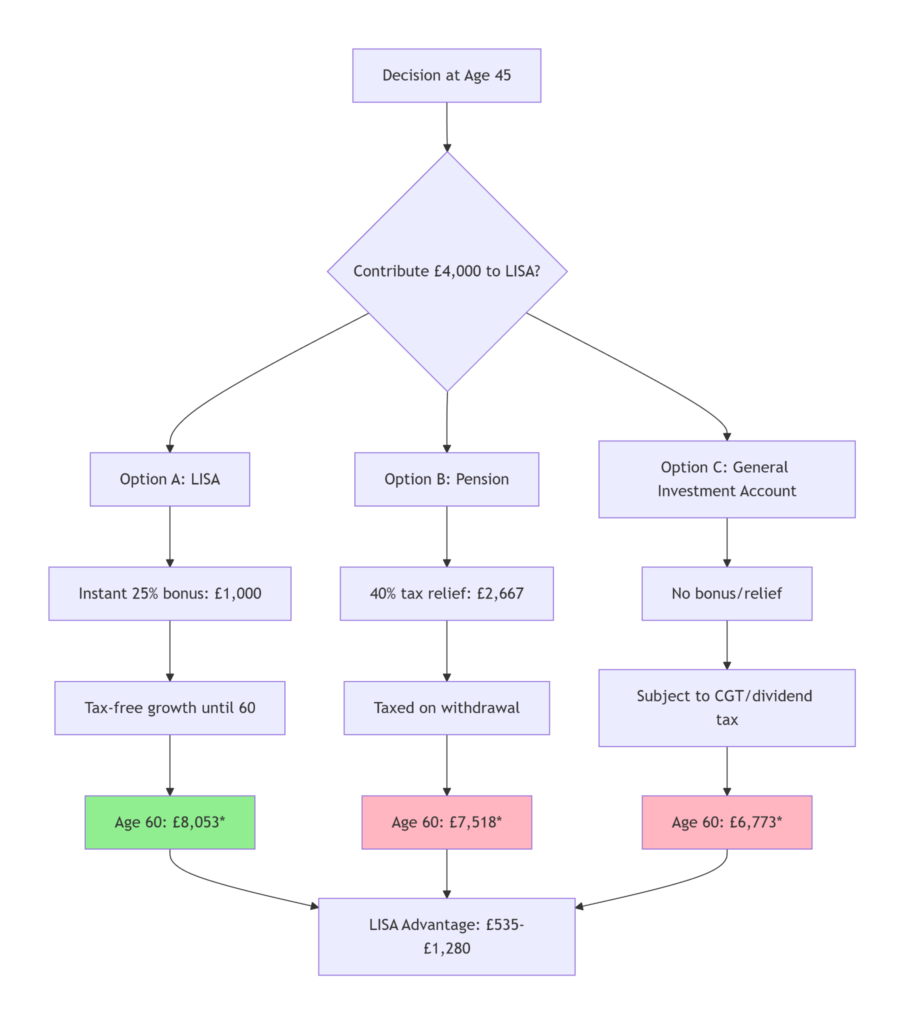

Scenario Analysis: Contributing £4,000 at Age 45

Assumes 5% annual growth, basic rate taxpayer in retirement

The Diminishing Time Horizon Effect

As retirement approaches, the LISA’s tax-free advantage competes with pensions’ earlier access:

| Contribution Age | Years to LISA Access | Years to Pension Access | Access Advantage |

| 40 | 20 years | 17 years (57) | Pension: 3 years |

| 45 | 15 years | 12 years | Pension: 3 years |

| 48 | 12 years | 9 years | Pension: 3 years |

| 49 | 11 years | 8 years | Pension: 3 years |

Key Insight: The closer you are to retirement, the more valuable early pension access becomes relative to LISA’s tax-free status.

Chapter 3: The First-Time Buyer Dilemma Over 40

The Growing Demographic Reality

With the average age of first-time buyers without parental help now 37 (rising to 41 in London), thousands approach their first purchase after the LISA opening window closes.

Regional Breakdown of First-Time Buyer Ages:

- London: 41 years

- South East: 38 years

- South West: 36 years

- Midlands: 35 years

- North: 34 years

- Scotland: 33 years

Alternatives for Over-40 First-Time Buyers

1. Help to Buy: Equity Loan (until March 2025)

- Eligibility: First-time buyers, any age

- Mechanism: 20% equity loan (40% London)

- Price cap: £600,000 (£450,000 London)

- Advantage: No interest for 5 years

2. Shared Ownership

- Eligibility: Household income <£80,000 (£90,000 London)

- Mechanism: Purchase 25-75% of the property

- Advantage: Lower deposit requirements

3. Retirement Interest-Only Mortgages

- For: Those approaching retirement

- Feature: Payments cover interest only

- Benefit: Lower monthly commitments

The “Bank of Family” Reality

For many over-40 first-time buyers, family assistance becomes crucial:

- 42% of first-time buyers over 40 receive family help (UK Finance)

- Average gifted deposit: £25,000

- Strategic approach: Combine family help with mortgage innovation

Chapter 4: The Retirement Focus – LISA vs Pension After 40

The Tax Efficiency Comparison for Over-40s

Higher Rate Taxpayers (40%):

£10,000 retirement contribution:

– SIPP: Costs £6,000 (gets £10,000 invested)

– LISA: Costs £10,000 (gets £12,500 invested)

– **Difference:** SIPP saves £4,000 now vs LISA’s £2,500 bonus

Net position after basic rate tax in retirement:

– SIPP: £8,500 (after 20% tax)

– LISA: £12,500 (tax-free)

– **LISA advantage:** £4,000

Basic Rate Taxpayers (20%):

£10,000 retirement contribution:

– SIPP: Costs £8,000 (gets £10,000 invested)

– LISA: Costs £10,000 (gets £12,500 invested)

– **Difference:** SIPP saves £2,000 now vs LISA’s £2,500 bonus

Net position after basic rate tax in retirement:

– SIPP: £8,500

– LISA: £12,500

– **LISA advantage:** £4,000

The Access Age Consideration

With pension access age rising to 57 in 2028, the gap between pension and LISA access narrows:

Current ages (2024):

– Pension access: 55 (rising to 57)

– LISA access: 60

– Difference: 5 years (reducing to 3)

For a 45-year-old:

– Pension access at: 57 (12 years)

– LISA access at: 60 (15 years)

– **Access advantage:** Pension by 3 years

The “LISA First” Strategy for Existing Holders

If you have an existing LISA and are deciding between additional contributions:

Priority order for over-40s:

1. Workplace pension to a maximum employer match

2. Existing LISA to £4,000 annually (if basic rate taxpayer)

3. SIPP for additional retirement savings

4. ISA for flexibility

Chapter 5: The Superior Alternatives – What Beats LISA After 40?

Alternative 1: Maximising Pension Contributions

The Annual Allowance Advantage:

- Standard allowance: £60,000 (2024/25)

- Carry forward: Unused allowance from the previous 3 years

- Potential contribution for over-40s: Up to £240,000 in one year

The Tax Relief Reality:

Higher rate taxpayer, age 45:

– £10,000 pension contribution

– Tax relief: £4,000

– NI savings via salary sacrifice: £1,380

– **Total saving:** £5,380

– Effective cost: £4,620 for £10,000 invested

Alternative 2: The Flexible ISA Strategy

Benefits Over LISA:

- No age restrictions

- No withdrawal penalties

- £20,000 annual allowance (vs LISA’s £4,000 within that)

- Same tax-free growth

- Immediate access if needed

The ISA Compounding Advantage:

text

Starting at 40 with £10,000 annual ISA contribution:

– By age 60: £347,192 (at 5% growth)

– All withdrawals are tax-free

– No access restrictions

Alternative 3: Venture Capital Trusts (VCTs) & EIS

For sophisticated investors over 40:

- VCTs: 30% income tax relief (minimum 5-year holding)

- EIS: 30% relief, loss relief, CGT deferral

- Risk: Higher, but tax benefits are substantial

- Suitability: Only for those comfortable with higher risk

Alternative 4: Property Investment via Limited Company

For those considering property as a retirement supplement:

- Mortgage interest is fully deductible

- Profits taxed at corporation tax rates (25% from April 2023)

- Extract profits via dividends or salary

- Consideration: Regulatory burden and market risk

Chapter 6: The Transfer Dilemma – What to Do With Existing LISAs

The Transfer Options Analysis

If you hold a LISA opened before 40, you face strategic decisions:

Option 1: Continue Contributions (Until 50)

- Maintains bonus eligibility

- Lock-in until 60 (or property purchase)

- Best for: Those certain of retirement use

Option 2: Transfer to ISA

- Process: Withdraw with 25% penalty, reinvest in ISA

- Maths: 6.25% loss of your contributions

- When sensible: If needing access before 60 and penalty < alternative costs

Option 3: Hold Without Further Contributions

- Money continues growing tax-free

- Access at 60 (or property)

- Minimal ongoing management

The “Penalty Break-Even” Calculation

To determine if penalty withdrawal makes sense:

Required alternative return = (Penalty % / Years to 60) + Alternative return

Example – Age 45, 15 years to LISA access:

– Penalty: 6.25% of contributions

– Annualised penalty cost: 0.42%

– If alternative investment returns >0.42% more than LISA, consider withdrawal

Chapter 7: The Couples Strategy – Maximising Household Benefits

The Age Disparity Advantage

Mixed-age couples can strategise effectively:

Scenario: Partner A (38), Partner B (42)

- Action: Partner A opens LISA immediately

- Maximum household bonus: £11,000 (if Partner A contributes 11 years)

- Property purchase: Can combine bonuses if both are first-time buyers

The Intergenerational Planning Opportunity

Parents over 40 can assist children’s LISAs:

- Gift money to adult children for LISA contributions

- Child receives 25% government bonus

- Potential inheritance tax advantages

- Limit: £3,000 annual gift allowance (£6,000 if unused previous year)

Chapter 8: The 2024 Economic Context – Inflation, Rates and Regulations

Interest Rate Environment Impact

With the Bank of England base rate at 5.25% (March 2024):

- Cash LISAs offer 3.5-4.25%

- Inflation at 3.4% creates minimal real returns

- Implication: Stocks & Shares LISA likely better for retirement-focused over-40s

The Abolition of Lifetime Allowance (2024 Budget)

Game-changing for over-40s:

- No tax charge on large pension pots

- The maximum tax-free lump sum remains £268,275

- Impact: Makes pensions more attractive for wealthier over-40s

Frozen Tax Thresholds Until 2028

- Personal allowance: £12,570 (frozen)

- Higher rate threshold: £50,270 (frozen)

- Result: More over-40s pushed into higher tax bands, enhancing pension relief value

Chapter 9: The Psychological Aspects – Behavioural Finance Insights

The “Sunk Cost” Fallacy

Many over-40s with existing LISAs feel compelled to continue contributions because they’ve “already started.” Behavioural economists call this the “sunk cost fallacy.”

Rational approach:

- Evaluate current contributions independently

- Ignore previous contributions in decision-making

- Consider whether you’d start today if new

The “Loss Aversion” to Penalties

The 25% withdrawal penalty triggers disproportionate psychological pain:

- Actual loss: 6.25% of your money

- Perceived loss: Often feels like 25%

- Result: Many hold LISAs sub-optimally to avoid penalty

The “Deadline Effect”

The age 50 contribution deadline creates artificial urgency:

- Leads to rushed decisions at 49

- May cause overallocation to LISA vs better options

- Antidote: Plan contributions from 40, not 49

Chapter 10: The Action Plan – A Decade-by-Decade Guide

Ages 40-44: The Strategic Assessment Phase

Annual Checklist:

- Review existing LISA performance

- Compare with pension contribution benefits

- Assess property purchase plans

- Calculate retirement income projections

- Consider partial LISA contributions if beneficial

Ages 45-49: The Maximum Contribution Phase

If keeping LISA:

- Maximise £4,000 annual contributions

- Ensure investments match the timeline

- Coordinate with pension contributions

If abandoning LISA:

- Calculate penalty vs opportunity cost

- Execute transfer in April (new tax year flexibility)

- Reinvest in the optimal vehicle

Ages 50+: The Growth & Transition Phase

Actions:

- No further LISA contributions allowed

- Monitor performance vs alternatives

- Plan a withdrawal strategy for age 60

- Consider partial withdrawals to manage taxes in retirement

The Five-Year Review Cycle

Every five years, over-40s should:

- Recalculate retirement projections

- Re-evaluate LISA vs alternatives

- Adjust investment strategy for changing timeline

- Review life circumstances and goals

- Optimise overall financial plan

Conclusion: Finding Value Beyond the Age Barrier

The LISA’s age restriction represents one of personal finance’s great ironies: just as many Britons achieve the financial stability and clarity to benefit from structured savings, the government withdraws one of its most generous incentives. Yet this closure reveals a more profound truth: sophisticated financial planning in your 40s transcends any single product.

The Three Core Realities for Over-40s:

- The LISA isn’t dead if you have one – Existing accounts remain potent tools, particularly for basic rate taxpayers planning retirement incomes below £50,000

- Pensions usually win for higher earners – The combination of higher relief, earlier access, and employer contributions typically overwhelms LISA benefits

- Flexibility has increasing value – As life complexity grows in your 40s and 50s, the ISA’s accessibility often outweighs LISA’s restrictions

The age 40 LISA deadline, while frustrating, serves as a valuable financial milestone—a prompt to reassess, recalibrate, and often discover that more powerful vehicles await those willing to look beyond a single product. In the words of financial planner Sarah Coles: “The best savings vehicle isn’t the one with the cleverest marketing or even the highest bonus—it’s the one that fits your actual life, not the life you imagined at 25.”

For Britain’s over-40s, that life is richer, more complex, and ultimately more financially promising than any age-restricted account could accommodate. Your best savings years aren’t behind you—they’re just taking a different, potentially more profitable, path.

Disclaimer: This article represents financial information, not personal advice. Tax rules, pension regulations, and product details change regularly. The LISA age restrictions, pension access ages, and tax thresholds are subject to government policy changes. Figures based on March 2024 data and assumptions. Past investment performance does not predict future returns. The value of investments can fall as well as rise. Always consult official government guidance and consider speaking with a qualified financial adviser before making financial decisions. Individual circumstances vary significantly, particularly for those over 40 with complex financial situations.