In the evolving landscape of UK retirement planning, two tax-efficient vehicles stand as potential champions for your golden years: the Self-Invested Personal Pension (SIPP) and the Lifetime ISA (LISA). With British households currently holding £1.2 trillion in personal pensions (ONS, 2024) and LISA balances surpassing £7.4 billion (HMRC, 2023), the choice between these options represents one of the most consequential financial decisions for savers under 50.

The pension freedoms revolutionised retirement access, while the LISA introduced unprecedented flexibility for younger savers. Yet this expansion of choice has created a modern dilemma: should you prioritise the traditional tax relief of pensions or embrace the accessible bonus structure of the LISA?

This comprehensive analysis dissects both vehicles through the lens of 2024’s economic realities, providing actionable insights for savers navigating Britain’s complex retirement landscape.

Chapter 1: The Fundamental Mechanics – Understanding the DNA of Each Vehicle

The SIPP: Traditional Power with Modern Flexibility

A Self-Invested Personal Pension is a pension wrapper offering investment choice and control. Unlike workplace pensions, you select the investments, provider, and contributions.

2024 SIPP Key Characteristics:

- Tax Relief: Basic rate (20%) added automatically; higher rates claimed via self-assessment

- Annual Allowance: £60,000 (reduced for high earners)

- Lifetime Allowance: ABOLISHED (Spring Budget 2024)

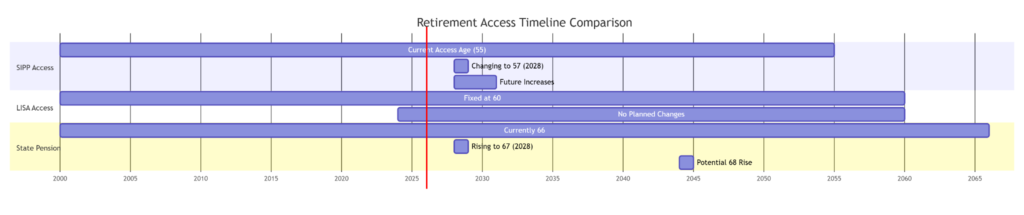

- Access Age: 55 (rising to 57 in 2028)

- Taxation: 25% tax-free lump sum, remainder taxed as income

The Tax Relief Mechanism:

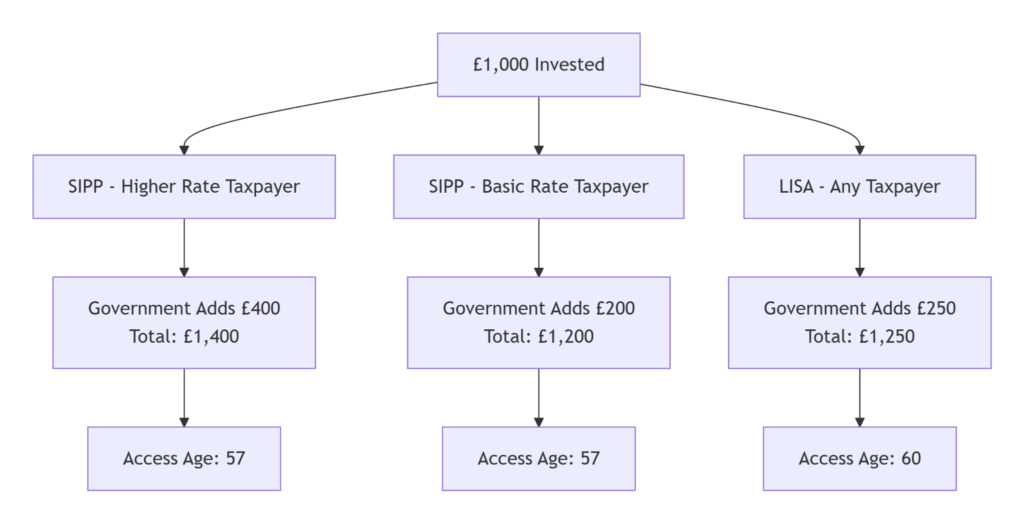

Basic Rate Taxpayer:

– Contribution: £800

– Tax Relief Added: £200

– Total Invested: £1,000

– Effective Cost: 80p per £1 invested

Higher Rate Taxpayer:

– Contribution: £600

– Tax Relief Added: £400

– Total Invested: £1,000

– Effective Cost: 60p per £1 invested

The LISA: The Newcomer with Youthful Appeal

The Lifetime ISA combines retirement and home-buying incentives in one package.

2024 LISA Key Characteristics:

- Bonus Structure: 25% on contributions (maximum £1,000 annually)

- Annual Limit: £4,000 (within £20,000 ISA allowance)

- Access Age: 60 (or first home purchase)

- Taxation: Completely tax-free withdrawals

- Age Restrictions: Open 18-39, contribute until 50

The Bonus Mechanics:

Annual Contribution: £4,000

Government Bonus: £1,000 (25%)

Total Invested: £5,000

Effective Return: Instant 25% gain

Chapter 2: The Mathematical Showdown – A Comparative Analysis

The Contribution Efficiency Matrix

Growth Projections: A 30-Year Case Study

Scenario: Sarah, age 30, £4,000 annual investment until 60, 5% annual growth

| Vehicle | Tax Status | Total Contributions | Gov. Addition | Age 60 Value | Tax on Withdrawal | Net After Tax |

| SIPP | Higher Rate | £120,000 | £80,000 | £398,633 | £119,590* | £279,043 |

| SIPP | Basic Rate | £120,000 | £30,000 | £348,804 | £68,702* | £280,102 |

| LISA | Any | £120,000 | £30,000 | £348,804 | £0 | £348,804 |

*Assumes 20% average tax in retirement, 25% tax-free lump sum taken

The Surprising Outcome: For basic rate taxpayers, the LISA delivers approximately £68,700 more net retirement income despite lower government contributions.

The Age Factor: When Time Changes Everything

The mathematical advantage shifts based on your age when contributions begin:

Starting Age 20 (40 years to retirement):

– LISA advantage: £4,000/year × 40 years = Maximum bonus capture

– SIPP advantage: Extra 3 years access (57 vs 60)

Starting Age 35 (25 years to retirement):

– LISA: Only 15 contribution years possible

– SIPP: Full allowance available until retirement

Chapter 3: Tax Efficiency Through the Retirement Lens

The Withdrawal Taxation Reality

SIPP Withdrawal Mechanics:

- 25% tax-free lump sum (up to £268,275 currently)

- Remainder taxed as income

- Flexible drawdown available

- 2024 Change: No lifetime allowance tax charge

LISA Withdrawal Mechanics:

- 100% tax-free from age 60

- No restrictions on withdrawal amounts

- Must be taken as cash (cannot remain invested)

The Marginal Rate Analysis

Your retirement tax bracket determines which vehicle shines:

| Retirement Income | Tax Rate | SIPP Efficiency | LISA Efficiency |

| Below £12,570 | 0% | High (25% tax-free) | Maximum |

| £12,571-£50,270 | 20% | Moderate | High |

| £50,271-£125,140 | 40% | Lower | Maximum |

| Above £125,140 | 45% | Lower | Maximum |

The Cross-over Point: Basic rate taxpayers retiring on £25,000 annual income might pay £2,486 tax on SIPP withdrawals. The same income from LISA: £0 tax.

The Inheritance Tax Considerations

SIPP Inheritance Rules:

- Passes outside the estate if nominated

- Beneficiaries pay income tax on withdrawals

- No inheritance tax is typically due

LISA Inheritance Rules:

- Forms part of the estate

- Spouse/civil partner can inherit ISA allowance

- Potentially subject to 40% inheritance tax

Chapter 4: Access & Flexibility – The Liquidity Equation

Access Timelines Compared

Early Access Penalties: A Critical Distinction

SIPP Early Access:

- Before 55 (57 from 2028): 55% unauthorised payment charge

- Exceptional circumstances only (terminal illness)

- Essentially inaccessible

LISA Early Access:

- Before 60 for non-property: 25% withdrawal charge

- Effectively 6.25% loss of your contributions

- Available for emergencies (with penalty)

The Flexibility Premium: LISA offers a penalty-based escape route; SIPP is effectively locked until pension age.

The Contribution Flexibility

SIPP Advantages:

- No upper age limit for contributions

- Carry forward unused allowance (3 years)

- Employer contributions possible

LISA Limitations:

- Cannot open after 39

- Cannot contribute after 50

- No employer contributions

- £4,000 annual cap

Chapter 5: Investment Choices & Control

Investment Universe Comparison

| Asset Class | SIPP Availability | LISA Availability |

| UK Shares | Extensive | Extensive |

| International Shares | Extensive | Extensive |

| Investment Funds | Full range | Full range |

| ETFs | Comprehensive | Comprehensive |

| Corporate Bonds | Yes | Yes |

| Government Gilts | Yes | Limited |

| Commercial Property | Via REITs/funds | Via REITs/funds |

| Direct Property | No | No |

| P2P Lending | Limited | Via IFISA separately |

Platform & Cost Analysis

Typical SIPP Costs (2024):

- Platform fee: 0.25%-0.45% annually

- Fund fees: 0.1%-0.8% depending on choice

- Trading fees: £5-£12 per trade (discount brokers are cheaper)

Typical LISA Costs:

- Often identical to ISA pricing

- Some providers offer free LISA accounts

- Investment fees similar to SIPP

The Economies of Scale: Larger portfolios often benefit from SIPP fixed-fee structures, while smaller portfolios might find LISAs cheaper.

Chapter 6: The 2024 Economic Context – How Current Conditions Influence Choice

Interest Rate Environment Impact

With the Bank of England base rate at 5.25% (March 2024):

- Cash LISAs offer 4.0-4.5%

- SIPP cash holdings typically earn less

- Implication: Short-term, risk-averse retirement savings might favour Cash LISA

Inflation Dynamics

Inflation at 3.4% (February 2024) affects both vehicles:

- Real returns become crucial

- Investment growth needed to outpace inflation

- Tax efficiency magnifies real returns

The Abolition of Lifetime Allowance

Spring Budget 2024 Game-Changer:

- Lifetime Allowance charge removed

- Maximum tax-free lump sum frozen at £268,275

- Impact: Makes larger SIPP pots more attractive for wealthier savers

The 2024/25 Tax Threshold Freezes

- Personal allowance frozen at £12,570 until 2028

- Higher rate threshold frozen at £50,270

- Result: More retirees pushed into tax brackets, enhancing LISA’s tax-free appeal

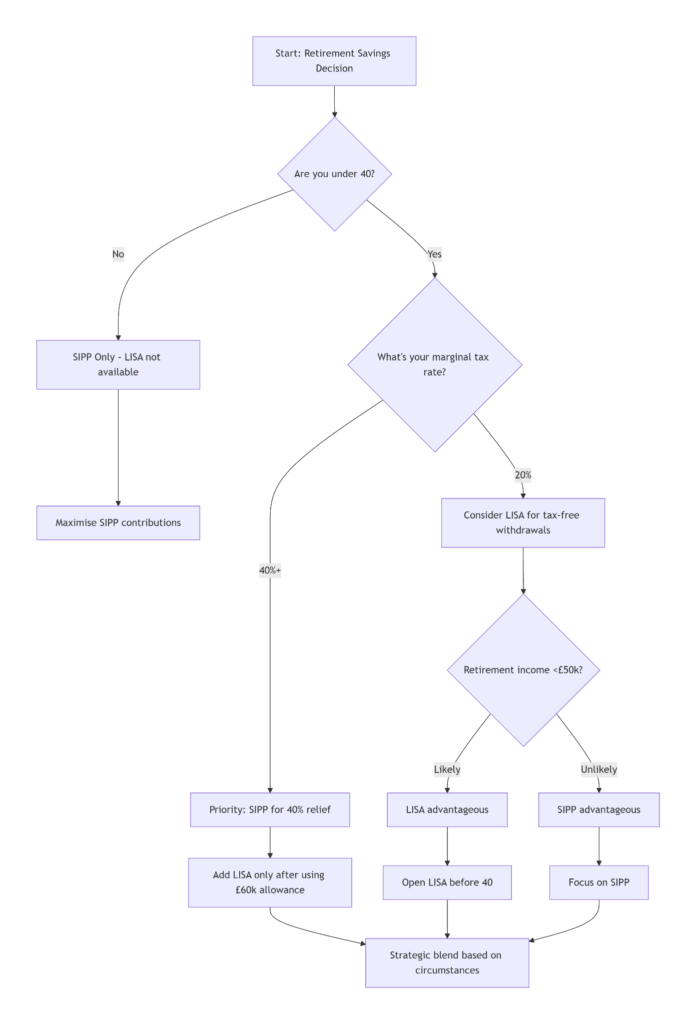

Chapter 7: Strategic Integration – The “Both/And” Approach

The Optimal Blending Strategy

Rather than choosing exclusively, consider strategic allocation:

For Basic Rate Taxpayers:

1. Employer pension to maximum match (free money)

2. LISA to £4,000 annually (tax-free growth)

3. Remaining to SIPP (additional tax relief)

For Higher Rate Taxpayers:

text

1. Employer pension to maximum match

2. SIPP to utilise 40% tax relief

3. LISA only if SIPP annual allowance used

Lifecycle Allocation Model

The Salary Sacrifice Consideration

Critical Insight: Workplace salary sacrifice pensions often beat both SIPP and LISA due to:

- Full National Insurance savings (13.8% employer + employee)

- Possible employer contribution matching

- Lower administrative costs

Example – £10,000 contribution:

- Salary sacrifice: Costs £5,800 (40% taxpayer + NI savings)

- SIPP: Costs £6,000 (40% relief, no NI savings)

- LISA: Costs £10,000 (25% bonus, no tax/NI savings)

Chapter 8: Demographic-Specific Recommendations

The Young Professional (25-30)

Characteristics: Basic rate taxpayer, uncertain home ownership plans

Recommendation:

- Open LISA immediately (age window closing)

- Contribute £1,000-£2,000 annually

- Use a workplace pension for the employer match

- Reassess at 35 based on property plans

The Mid-Career Accelerator (35-45)

Characteristics: Higher rate taxpayer, home owned, retirement focused

Recommendation:

- Maximise SIPP contributions first

- Consider LISA only after using the pension annual allowance

- Utilise salary sacrifice if available

- Prioritise tax relief over accessibility

The Self-Employed Professional

Characteristics: Variable income, no employer contributions

Recommendation:

- LISA for stability and accessibility

- SIPP for larger, irregular contributions

- Consider timing contributions to higher tax years

The Part-Time Worker with Multiple Jobs

Characteristics: Multiple employments, each below the auto-enrolment threshold

Recommendation:

- LISA as primary vehicle

- Opt into workplace pensions if beneficial

- Consolidate pension pots regularly

Chapter 9: Common Pitfalls & How to Avoid Them

Pitfall 1: The Tax Relief Mismatch

Scenario: Higher rate taxpayer chooses LISA over SIPP

Loss Calculation:

- £4,000 in LISA: £1,000 bonus

- £4,000 in SIPP: £2,000 tax relief (gross £6,667 contribution)

- Annual loss: £1,000 in government contribution

Avoidance: Always calculate the effective government addition based on your tax rate.

Pitfall 2: The Age Window Miss

Scenario: Waiting until 40 to consider LISA

Consequence: Permanently locked out of £33,000 potential bonuses

Solution: Open LISA with a token amount before 40, even if not funding immediately.

Pitfall 3: The Liquidity Overlook

Scenario: Loading LISA, then needing funds before 60

Penalty Reality: 25% withdrawal charge = 6.25% loss of your money

Mitigation: Maintain a separate emergency fund before maximising LISA.

Pitfall 4: The Employer Match Neglect

Scenario: Contributing to a personal pension instead of a workplace scheme

Loss: 100%+ immediate return from employer contributions

Rule: Always maximise employer match before any other retirement savings.

Chapter 10: The 2024 Decision Framework

The Decision Tree

The Five Critical Questions:

- What’s your current marginal tax rate? (Determines relief value)

- At what age will you access retirement funds? (57 vs 60)

- What’s your expected retirement income? (Tax bracket in retirement)

- Do you have workplace pension matching? (Free money first)

- Are you certain about not needing funds before retirement? (Liquidity needs)

The Emergency Fund Precondition

Before contributing to either vehicle:

- Build 3-6 months’ expenses in accessible savings

- Ensure you’re not accumulating high-interest debt

- Consider short-term goals (next 5 years)

Conclusion: Beyond Binary Choices to Strategic Synthesis

The SIPP versus LISA debate ultimately reveals a nuanced truth: for most UK savers, the optimal strategy involves both vehicles deployed at different life stages for different purposes.

The 2024 Synthesis Strategy:

- Ages 18-39: Open LISA with minimum funding to secure an option

- Throughout working life: Maximise workplace pension with employer match

- Higher rate taxpayers: Prioritise SIPP to capture 40%+ relief

- Basic rate taxpayers: Seriously consider LISA for tax-free withdrawals

- Ages 40+: Focus on SIPP and pension consolidation

- Always: Maintain liquidity outside retirement wrappers

The Final Arithmetic Reality:

- For a basic rate taxpayer retiring on £30,000 annual income, the LISA typically delivers 15-25% more net income than an equivalent SIPP

- For a higher-rate taxpayer with substantial retirement income, the SIPP’s upfront relief usually triumphs

- For everyone, employer pension matching represents a non-negotiable priority

As former Pensions Minister Sir Steve Webb notes: “The LISA introduced valuable flexibility for younger savers, but it complements rather than replaces our pension system. The savvy saver uses each tool where it fits their personal tax and timeline picture.”

Your retirement journey will likely span both vehicles at different times. The critical insight isn’t choosing one forever, but understanding when each serves your evolving financial landscape best. In 2024’s complex savings environment, that strategic flexibility might be the most valuable retirement asset of all.

Disclaimer: This article represents financial information, not personal advice. Tax rules, pension regulations, and economic conditions change regularly. The abolition of the Lifetime Allowance, pension access ages, and LISA rules is subject to government policy changes. Figures based on March 2024 data and assumptions. Past investment performance does not predict future returns. The value of investments can fall as well as rise. Always consult the official government guidance and consider speaking with a qualified financial adviser before making retirement planning decisions. Pension and retirement planning depend on individual circumstances.