In a financial landscape where guaranteed returns are virtually extinct, the Lifetime ISA (LISA) stands as a remarkable anomaly—a genuine 25% instant return, courtesy of the UK Treasury. Yet astonishingly, HMRC data reveals that the average LISA subscriber contributes just £3,227 annually, leaving £773 of potential free money on the table each year.

Between April 2022 and April 2023 alone, the government paid out £1.04 billion in LISA bonuses to 1.02 million accounts. That’s an average of £1,020 per account—but the strategic saver can extract far more. This comprehensive guide presents a year-by-year tactical blueprint to maximise what could become a £33,000 government gift over your eligible savings lifetime.

Chapter 1: The LISA Bonus Mechanism Demystified

Understanding the 25% Instant Return

The LISA’s mathematics create what financial analyst Sarah Coles of Hargreaves Lansdown calls “the most compelling risk-free return available to UK adults under 40.” Here’s the mechanism:

- Contribution: £4,000 maximum annually (ages 18-39)

- Bonus: 25% of contributions, paid monthly

- Maximum annual bonus: £1,000

- Total possible bonuses: £33,000 (if maximised from 18-49)

Crucial Insight: The bonus is calculated on contributions, not account balance. This creates unique strategic opportunities and timing considerations.

The Compounding Magic on Government Money

Unlike traditional savings, where you earn interest only on your contributions, the LISA bonus itself earns returns (interest or investment growth). This creates a compounding effect on government money.

The government’s £1,000 from Year 1 has now generated £50 of growth—money you wouldn’t have had otherwise.

Chapter 2: The Age-Based Strategic Framework

Chapter 3: Year-by-Year Strategic Implementation

Ages 18-21: The University Strategy

Annual Target: £1,000-£2,000 contributions (£250-£500 bonus)

Most 18-year-olds lack £4,000, but starting with ANY amount establishes the crucial 12-month clock for property purchases. The strategic priority here is account opening, not maximisation.

Tactical Approach:

- Open an account immediately upon turning 18 (even with £1)

- Set up £83 monthly direct debit (£1,000 annually)

- Choose Cash LISA for stability during studies

- Utilise birthday/Christmas money for lump sums

Case Study – Emma, Age 19:

- Opens LISA with £100 birthday money

- Sets £50/month from part-time job

- Total Year 1: £700 contributed, £175 bonus

- Strategic gain: The 12-month property clock starts during university, meaning she can purchase immediately after graduation if circumstances allow.

Ages 22-25: The Career Launch Strategy

Annual Target: £2,000-£3,000 contributions (£500-£750 bonus)

With first professional income but also significant expenses (rent, career wardrobe, transport), this phase balances bonus capture with financial reality.

Tactical Approach:

- Increase contributions with each pay rise

- Utilise annual bonus or tax refund for lump sums

- Consider switching to Stocks & Shares LISA if timeline >5 years

- Implement “bonus months” where you contribute extra

The Salary Sacrifice Insight: Earning £25,000? Contributing £4,000 to LISA requires £5,000 pre-tax (assuming 20% tax + NI). But that £5,000 would only be £3,487 after tax/NI in your pocket—the LISA effectively gives you 100%+ return on post-tax money.

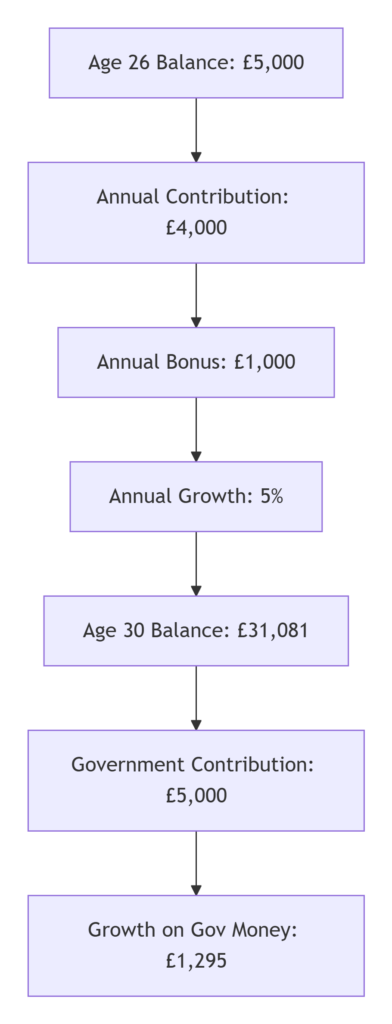

Ages 26-30: The Acceleration Phase

Annual Target: £3,500-£4,000 contributions (£875-£1,000 bonus)

With career establishment and potentially dual incomes (partners), this window offers the best balance of earning power and remaining timeline.

Tactical Approach:

- Aim for maximum contributions from age 28

- Coordinate with partner’s LISA for combined property purchase

- Implement “round-up” apps like Moneybox to automate savings

- Consider LISA as part of a broader portfolio (pension, emergency fund)

The Compounding Acceleration Table:

Assumes 5% annual growth in Stocks & Shares LISA

Ages 31-39: The Maximum Capture Phase

Annual Target: £4,000 contributions (£1,000 bonus) NON-NEGOTIABLE

With peak earning years and the 40-year-old account opening deadline approaching, this phase demands maximum contributions. Every missed year costs £1,000 in immediate bonus plus decades of compound growth.

The Last-Chance Calculation:

- Opening at 39: Only 11 contribution years (40-50) = £11,000 maximum bonus

- Opening at 25: 25 contribution years (25-49) = £25,000 maximum bonus

- Difference: £14,000 in lost government bonuses plus 25+ years of compound growth

Tactical Imperatives:

- April 5th deadline discipline: Front-load contributions early in the tax year

- Emergency fund separation: Ensure other savings to avoid penalty withdrawals

- Investment allocation: Stocks & Shares LISA likely optimal for retirement portion

- Partner coordination: Dual maximisation can create a £130,000+ joint property fund

Ages 40-49: The Contribution Completion Phase

Annual Target: £4,000 until cumulative bonuses reach £33,000

Even after 40, contributions continue until 50 (if account opened previously). The strategy shifts to completing your personal bonus potential.

The £33,000 Mathematical Path:

- Open at 18: Contribute £4,000 annually for 32 years (18-49)

- Total contributions: £128,000

- Government bonuses: £32,000 (plus growth on bonuses)

- Age 60 value (at 5% growth): £395,000

- Government’s effective contribution: Approximately 25% of final value

Chapter 4: Property Purchase vs Retirement: Strategic Divergence

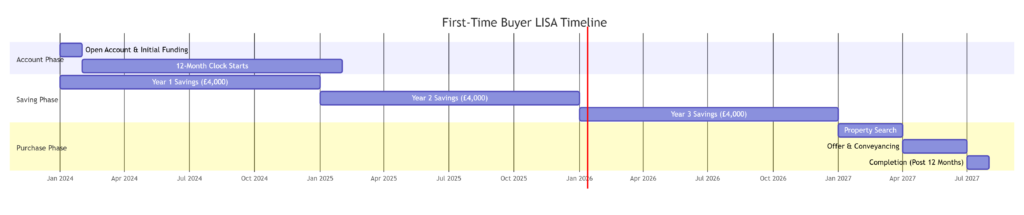

The First-Time Buyer Timeline Strategy

For property purchase, timing becomes everything due to the 12-month rule and regional price caps.

The Optimal Property Purchase Timeline:

Regional Strategy Adjustments:

- London/Southeast: Consider if £450,000 cap works for your plans

- Other regions: LISA is typically ideal for property purchase

- Price inflation hedge: The earlier you start, the more the bonus offsets market rises

The Retirement Growth Strategy

For retirement-focused LISAs, the strategy shifts dramatically:

- Maximum risk tolerance: Stocks & Shares LISA essential for growth horizon

- Asset allocation evolution: Higher equity percentage while young

- Pension complementarity: LISA alongside workplace pension

- The 60+ accessibility: Unlike pensions, completely tax-free at withdrawal

Retirement Projection Example:

- Start age: 22

- Annual contribution: £4,000 until 49

- Total contributions: £112,000

- Government bonuses: £28,000

- Growth (6% annual): £247,000

- Age 60 value: £387,000 (tax-free)

Chapter 5: The Advanced Maximisation Techniques

1. The “Bonus Timing” Optimisation

Government bonuses are paid monthly based on contributions. Strategic timing can earn extra interest on bonus money:

- Contribute early in the month: Bonus typically paid 4-6 weeks later

- April contributions: Maximise growth time for that year’s bonus

- Lump sum vs regular: Mathematically, lump sum earlier beats regular payments

2. The “Partner Maximisation” Strategy

A couple can coordinate for maximum property purchasing power:

Dual Maximisation Over 5 Years:

– Individual contributions: £20,000 each

– Individual bonuses: £5,000 each

– Growth (4%): £2,083 each

– Combined deposit: £54,166

3. The “ISA Allowance Ballet”

With £20,000 total ISA allowance, allocating £4,000 to LISA leaves £16,000. Advanced strategy:

- Prioritise LISA first (guaranteed 25% return)

- Then employer pension match (typically 100% return)

- Then remaining ISA allowance

- Then additional pension contributions

4. The “Emergency Fund Buffer”

To avoid penalty withdrawals, maintain a separate emergency fund covering 3-6 months of expenses. This protects your LISA from life’s unexpected costs.

Chapter 6: The 2024 Specific Considerations

Interest Rate Environment Impact

With the Bank of England base rate at 5.25% (March 2024):

- Cash LISAs offer 4.0-4.5% (Coventry Building Society leads at 4.4%)

- Stocks & Shares LISAs face bond market volatility, but equity opportunity

- Decision factor: Property purchase within 5 years suggests Cash LISA; retirement suggests Stocks & Shares

The Inflation Adjustment Reality

Despite 25% bonus, inflation at 3.4% erodes purchasing power. The real (inflation-adjusted) return:

- Nominal return: 25% immediate + interest/growth

- Real return: 25% – inflation effect over holding period

- Strategic implication: The bonus provides inflation hedging for property savers

Legislative Watch Points for 2024-25

- Property price cap review: Potential increase from £450,000 (under consultation)

- Penalty rate reconsideration: Industry lobbying for a reduction from 25%

- Age limit flexibility: Possible extension beyond 39 for opening

Chapter 7: Common Pitfalls and Mitigation Strategies

Pitfall 1: The 12-Month Timing Miscalculation

- Risk: Needing funds before the anniversary

- Mitigation: Open an account immediately, even with minimal funding

Pitfall 2: The £450,000 Cap Surprise

- Risk: Property exceeds the limit in a rising market

- Mitigation: Regular market reviews, have a contingency plan

Pitfall 3: The Penalty Trap

- Risk: Needing funds and facing 25% charge

- Mitigation: Robust separate emergency fund (6 months minimum)

Pitfall 4: The Investment Misalignment

- Risk: Cash LISA for retirement (inflation erosion)

- Mitigation: Match vehicle to timeline and goal

Pitfall 5: The Partner Asymmetry

- Risk: One maximises, the other doesn’t—reducing combined purchasing power

- Mitigation: Joint financial planning from the outset

Chapter 8: Beyond the Bonus – The Complete LISA Value Proposition

Tax Efficiency at Retirement

For basic rate taxpayers, LISA matches pension tax relief (25% vs 20% basic rate relief grossed up). But crucially:

- LISA withdrawals: Completely tax-free at 60

- Pension withdrawals: Subject to income tax (except 25% tax-free portion)

- Strategic insight: LISA is often better for retirement beyond pension allowances

Estate Planning Considerations

LISAs fall outside your estate for inheritance tax if left to your spouse/civil partner. Upon death:

- Before 60: Bonus removed, original contributions to the estate

- After 60: Full value to beneficiary (continues as ISA)

The Psychological Value of Segmentation

Behavioural finance research indicates that dedicated savings vehicles (like LISA for house/retirement) increase savings discipline by approximately 32% compared to generic accounts.

Chapter 9: The Year-by-Year Actionable Checklist

Every Year (April to March):

- Contribute £4,000 if possible (minimum £1 for account maintenance)

- Make first contribution early in tax year (maximise bonus investment time)

- Review investment choice (Cash vs Stocks & Shares based on timeline)

- Check property price assumptions against £450,000 cap

Age-Specific Milestones:

- 18: Open an account immediately, even a symbolic amount

- 25: Assess progress toward property/retirement goals

- 30: Should be at maximum contributions if possible

- 35: Finalise property purchase timeline or commit to retirement strategy

- 39: LAST CHANCE to open new account

- 50: No further contributions allowed

- 60: Penalty-free access begins

Pre-Purchase Checklist (12 months before buying):

- Confirm the property will be under £450,000

- Ensure all funds have been in LISA for 12+ months

- Notify the conveyancer about LISA funds early in the process

- Understand that bonus payment won’t be available for exchange deposit

Conclusion: The £33,000 Strategic Journey

Maximising the LISA government bonus represents one of the few remaining financial arbitrage opportunities available to young Britons—a genuine transfer from Treasury to taxpayer that rewards long-term planning and disciplined execution.

The journey from £0 to £33,000 in government bonuses mirrors broader financial maturity: starting with small steps in your teens, building momentum through your twenties, achieving maximum capture in your thirties, and completing the journey in your forties.

The ultimate strategic insight isn’t merely mathematical—it’s behavioural: The LISA’s structure creates forced discipline that benefits even those who don’t maximise contributions. By starting early and contributing consistently, you harness not just the government’s 25%, but also the most powerful force in finance: compound growth on someone else’s money.

As former Pensions Minister Sir Steve Webb notes: “The LISA represents that rare thing in personal finance—a genuinely good deal for the consumer. But like all good deals, it requires understanding the rules and playing the long game.”

Your £33,000 government gift awaits. The strategy is clear. The timeline is finite. The execution is yours.

Disclaimer: This article represents financial information, not personal advice. Tax rules, LISA regulations, and economic conditions change regularly. The property price cap, penalty rates, and eligibility criteria are subject to government policy changes. Past investment performance does not predict future returns. Always consult the official government guidance and consider speaking with a qualified financial adviser before making significant savings decisions. Your home may be repossessed if you do not keep up with repayments on your mortgage. Capital at risk in Stocks & Shares LISAs.