In the world of UK personal finance, the Lifetime ISA (LISA) presents a tantalising proposition: an instant 25% government bonus on your savings. Yet behind this generous incentive lies one of the most punitive penalty regimes in British savings history. Since April 2017, HMRC has collected £223 million in LISA penalties from distressed savers who stumbled over the fine print.

The latest data reveals a sobering reality: approximately 1 in 7 LISA holders will face the dreaded 25% withdrawal charge at some point, according to MoneyHelper’s 2024 analysis. With the average penalty amounting to £625 per withdrawal, understanding these rules isn’t just advisable—it’s financially essential.

This comprehensive guide dissects every LISA rule that can trigger penalties, offering practical strategies to navigate what financial journalists have dubbed “the bonus trap.”

Chapter 1: The Penalty Mathematics – Why 25% Doesn’t Mean What You Think

The Great Misunderstanding

Ask most LISA holders about the penalty, and they’ll confidently state “25%.” Few realise they’re quoting the wrong figure. The government’s 25% charge applies to the total withdrawal amount, creating a mathematical reality that sees savers losing their own money.

The Penalty Calculation Exposed:

The Hidden Compound Cost

The true cost multiplies when you consider lost growth. That £1,000 contribution could have been earning 5% elsewhere. Over five years, the effective loss approaches 35% of potential value when accounting for opportunity cost.

Real-World Example – Sarah’s Story:

- Age 25: Contributes £4,000, receives £1,000 bonus

- Age 26: Emergency requires a £5,000 withdrawal

- Penalty paid: £1,250

- Receives: £3,750

- Actual loss: £250 of her money + £1,000 bonus

- Opportunity cost: Potential growth on £5,000 at 4% for 10 years = £2,400

- Total effective loss: £2,650

Chapter 2: The Five Unbreakable Rules – A Compliance Checklist

Rule 1: The 12-Month Minimum Holding Period

The Rule: Funds must remain in your LISA for at least 12 months before being used for a first home purchase.

The Reality: The clock starts from your first contribution, not account opening. Many assume funding with £1 starts the clock—it doesn’t.

Compliance Strategy:

- Fund immediately with a meaningful amount

- Mark the calendar for the 12-month anniversary

- Consider this timeline before property searching

Case Study – The Premature Purchaser:

James opened his LISA in January 2023 with £1. He contributed £4,000 in March 2023. Finding his dream home in December 2023, he assumed he could use the funds. Result: Only the £1 from January qualified. The £4,000 faced penalties if withdrawn.

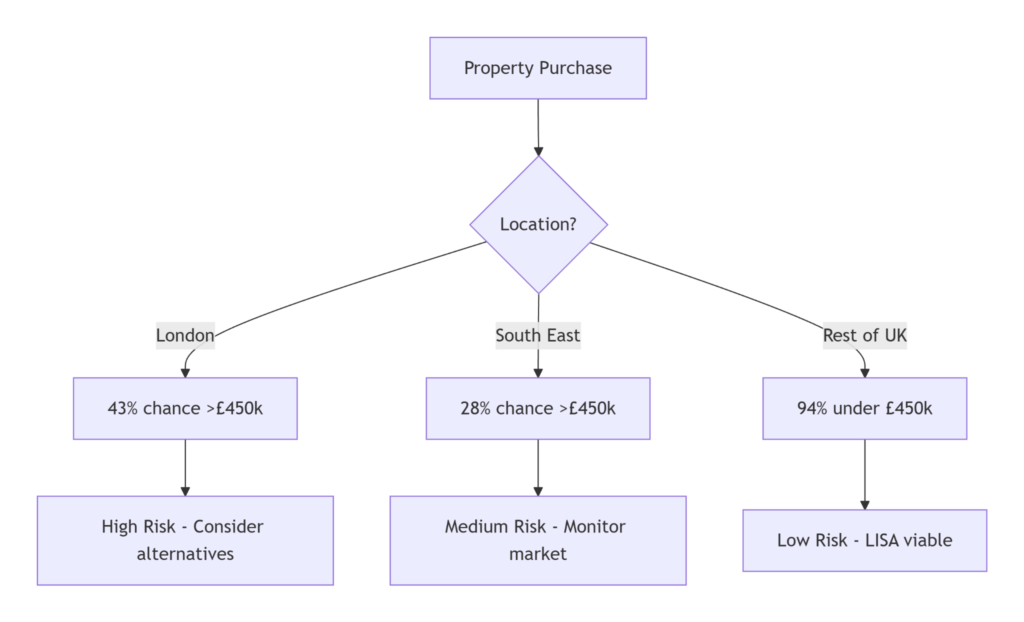

Rule 2: The £450,000 Property Price Cap

The Rule: The property must cost £450,000 or less.

The 2024 Reality: With average London flats now at £510,000 (Rightmove, Q1 2024), this cap excludes 43% of first-time buyers in the capital, according to UK Finance data.

Regional Compliance Map:

Mitigation Strategy:

- Regular price monitoring in the target area

- Have a non-LISA savings buffer if prices rise

- Consider regional variations (cap applies UK-wide)

Rule 3: The First-Time Buyer Definition

The Rule: You cannot have owned residential property anywhere in the world.

The Grey Areas That Trap Savers:

- Inherited property (even if sold)

- Property owned through a trust

- Overseas ownership (holiday homes abroad)

- Former ownership with a partner

The ‘Never Had a Mortgage’ Myth: Ownership matters, not mortgages. If you inherited 1% of a property, you’re disqualified.

Compliance Action:

- Complete HMRC’s first-time buyer declaration honestly

- Seek legal advice if any property history exists

- Disclose all global property interests

Rule 4: The Age-Based Contribution Window

The Rule:

- Open: 18-39 only

- Contribute: Until age 50

- Withdraw penalty-free: From age 60

The Birthday Trap: If you turn 40 on June 15th, your final opening day is June 14th. HMRC uses exact dates, not “in your 40th year.”

Strategic Implications:

- Age 38-39: Last chance opening requires maximum contributions to justify

- Age 49: Final contribution year – plan December payments to maximise

Rule 5: The Qualifying Withdrawal Conditions

Permitted Reasons (No Penalty):

- First residential property purchase (£450k or less)

- Reaching age 60

- Terminal illness (less than 12 months of life expectancy)

- Death (beneficiaries receive funds)

Everything Else Triggers 25% Charge:

- Job loss

- Medical emergencies (non-terminal)

- Relationship breakdown

- Business opportunities

- Education costs

- Caring responsibilities

Chapter 3: The Penalty Exceptions – Limited Escape Routes

The Terminal Illness Provision

The most overlooked exception: those diagnosed with less than 12 months to live can withdraw penalty-free. Documentation from a registered medical professional is required.

Process:

- Obtain medical certification

- Complete HMRC withdrawal form

- Submit to the LISA provider

- Typical processing: 2-4 weeks

The Death Transfer Rule

Upon death, the LISA:

- Bonus is removed

- Remaining contributions go to the estate

- No penalty applies

- Can be transferred to the spouse’s ISA allowance

The ‘Severe Financial Hardship’ Myth

Contrary to popular belief, there is no financial hardship exception. Redundancy, debt, or housing crisis don’t qualify. This catches out thousands annually.

Chapter 4: The Property Purchase Process – A Step-by-Step Penalty Avoidance Guide

Timeline for Penalty-Free Withdrawal:

Critical Documentation Requirements:

- Conveyancer’s Details: Must be UK-regulated

- Property Particulars: Address and purchase price

- First-Time Buyer Declaration: Signed statement

- Completion Date Confirmation: Must be provided

The Exchange-Completion Trap:

The Problem: LISA funds cannot be used for exchange deposits (except in Scotland). You need separate funds for the 10% deposit typically required at exchange.

Solution: Maintain non-LISA savings equivalent to 10% of the purchase price for exchange.

The Three-Party Dance:

- You request withdrawal from the provider (4-6 weeks before completion)

- Provider sends funds to conveyancer

- Conveyancer holds until completion day

Common Failure Point: Late withdrawal requests. Start the process the day your offer is accepted.

Chapter 5: The Investment vs Cash Decision – How Choice Affects Penalty Risk

Cash LISA Penalty Profile:

- Predictable value: Know exactly what you’ll lose if penalised

- Lower growth: May not outpace inflation

- Best for: Property purchase within 5 years

- Market risk: Penalty applied to current value, which may be below contributions

- Higher growth potential: Better for retirement timeline

- Double loss risk: Market downturn + penalty

The Market Crash Scenario:

- Invested: £4,000

- Bonus: £1,000

- Market falls 20%: Value = £4,000

- Penalty (25%): £1,000

- Received: £3,000

- Total loss: £1,000 (25% of original) + opportunity cost

The 2024 Interest Rate Consideration:

With best Cash LISAs paying 4.4% (Coventry Building Society, March 2024) and inflation at 3.4%, the penalty risk must be weighed against:

- Real returns on cash (1%)

- Alternative savings options

- Your certainty of meeting the LISA criteria

Chapter 6: The Strategic Withdrawal Considerations

When Taking the Penalty Might Make Sense

Scenario Analysis: Earning £60,000 and needing funds for a business opportunity returning 20% annually.

- Penalty cost: 6.25% of original capital

- Investment return: 20% annually

- Net gain: 13.75% after one year

The Mathematical Break-Even:

text

Required return = Penalty % + Alternative return

If cash savings earn 5%: Need >11.25% return to justify penalty

The ‘Strategic Loss’ Calculation:

Sometimes accepting the penalty is optimal:

- Property will exceed £450,000 cap

- Changed life plans (emigration, career change)

- Higher-return investment opportunity

- Avoiding higher-cost debt

Case Study – The Cap Breaker:

Maya, 28, saved £20,000 + £5,000 bonus for London flat. Prices rose; nothing available under £475,000. Options:

- Option A: Keep until 60 (32 years), grows to £147,000 at 5%

- Option B: Take penalty now, invest elsewhere

- Option C: Buy £475,000 with penalty + additional funds

She chose Option C, accepting £1,562 penalty to access £23,438 deposit.

Chapter 7: The Partner Considerations – Dual Account Pitfalls

Joint Purchase Rules:

- Both must be first-time buyers

- Both LISAs must meet the 12-month rule individually

- The combined bonus can be used

- One partner’s disqualification voids both bonuses

The Age Disparity Trap:

Partner A (38) and Partner B (42):

- Partner A can open LISA

- Partner B cannot (over 39)

- Result: Lost bonus potential on half the purchase

The Separation Scenario:

Couple with joint LISA plans separate:

- Individual penalties apply if withdrawn for non-property

- No ‘relationship breakdown’ exception exists

- Planning advice: Consider postponing LISA funding until the relationship is stable

Chapter 8: The 2024 Regulatory Landscape

Current Consultation – Potential Changes:

The Treasury’s 2023 LISA review identified several issues:

- Penalty rate reduction from 25% to 20% (reclaims just the bonus)

- Property cap increase to £500,000+ with regional variations

- Limited hardship exceptions for specific circumstances

Industry Position (Finance & Leasing Association):

“Maintain bonus integrity while reducing genuine hardship cases.”

Consumer Group Position (Which?):

“Penalty should only reclaim government contribution, not penalise savers.”

The Scottish Exception:

Unique to Scotland: LISA funds can be used for exchange deposits. This creates a UK asymmetry that many aren’t aware of.

The Conveyancer Compliance Requirement:

Since 2021, all conveyancers must complete HMRC-approved training on LISA withdrawals. Non-compliant conveyancers can delay the process by weeks.

Chapter 9: The Penalty Avoidance Action Plan

Pre-Funding Checklist:

- Confirm first-time buyer status (global check)

- Research property prices in the target area

- Establish a 6-month emergency fund separately

- Understand the partner’s position if applicable

- Choose Cash vs Stocks & Shares based on timeline

Annual Compliance Review:

- Verify property prices are still under £450,000 in the target area

- Confirm life circumstances haven’t changed eligibility

- Check contribution timing (avoid last-minute payments)

- Review investment choice against the timeline

The Emergency Fund Buffer:

Recommended: 6 months’ expenses in instantly accessible non-LISA savings. This should cover:

- Job loss period

- Unexpected costs

- Relationship changes

- Family emergencies

Calculation Example:

- Monthly expenses: £1,800

- 6-month buffer: £10,800

- Priority: Build this before maximising LISA contributions

The Gradual Funding Strategy:

Rather than £4,000 lump sum:

- Month 1: £500 + emergency fund building

- Month 2-12: £291 monthly to reach £4,000

- Benefit: Spreads risk, builds a buffer simultaneously

Chapter 10: When Things Go Wrong – The Penalty Management Guide

The Withdrawal Process:

- Contact the provider – Request penalty withdrawal form

- Complete declaration – Acknowledge penalty understanding

- Receive reduced funds – Typically within 10 working days

- Tax implications – No additional tax on withdrawn amounts

The Dispute Process:

If you believe a penalty was incorrectly applied:

- Formal complaint to provider (within 6 months)

- Financial Ombudsman if unsatisfied (within 6 months of final response)

- Success rate: Approximately 22% of LISA complaints upheld (FOS 2023 data)

The Recovery Strategy:

After penalty withdrawal:

- Document learning – What rule was missed?

- Rebuild emergency fund – Priority before more investing

- Consider alternatives – Help to Buy, LISA if still eligible

- Tax efficiency check – Other ISA allowances still available

Conclusion: Respecting the Rules to Harvest the Reward

The LISA represents a social contract between saver and state: substantial government generosity in exchange for strict behavioural compliance. The £223 million in collected penalties demonstrates how frequently this contract is breached, often through misunderstanding rather than malfeasance.

The fundamental insight emerging from a decade of LISA operation is this: The product works beautifully for those whose lives follow predictable patterns—steady employment, traditional property progression, linear career paths. It penalises those facing life’s inevitable curveballs: economic shifts, regional price movements, and personal circumstances changes.

Three Final Safeguards for Every LISA Holder:

- The Certainty Principle: Only commit funds you’re 90%+ certain will be used for qualifying purposes

- The Buffer Rule: Maintain equivalent non-LISA savings to your contributions for the first three years

- The Annual Review: Every April, reassess your life trajectory against LISA requirements

As Martin Lewis’s MoneySavingExpert team concludes in their 2024 LISA guide: “The bonus is real, the penalties are real, and the gap between them is where financial planning either succeeds or fails spectacularly.”

The £33,000 potential government gift remains available—but it’s guarded by rules that demand respect, understanding, and strategic navigation. Your journey to claiming it begins with knowing exactly where the tripwires lie.

Disclaimer: This article represents financial information, not personal advice. Tax rules and LISA regulations change regularly. The penalty rate, property cap, and eligibility criteria are subject to government policy changes. Figures based on March 2024 data and regulations. Past performance does not predict future returns. Always consult the official government guidance and consider speaking with a qualified financial adviser before making savings decisions. Your home may be repossessed if you do not keep up with repayments on your mortgage. Capital at risk in Stocks & Shares LISAs.